The doomsayers will have to wait further for their collapse scenarios on China finally to materialize. The World Bank has just lifted its 2017 forecast for economic growth in China amid rising household incomes and a recovery in global trade[1].

China’s and India’s high growth has boosted

global growth in recent years (Figure 1). From 2011 to 2015, China’s relative

contribution to global growth was on a par with advanced countries, despite its

per capita GDP growth falling from a top rate of 13.6 % in 2007 to 6.1 % in

2016. India’s contribution to global growth has also risen since the early

2000s, on the back of a per capita income growth rate oscillating between 8.8 %

in 2010 and 5.9% in 2016. However, China has contributed almost 30% to global growth

in recent years, approximately 20 percentage points more than India. As India

is still considerably poorer than China, it cannot yet offset the impact of

China’s slowdown on global growth and trade.

Figure 1: Contribution

to global growth, 1991-2015, by areas (%)

Source: AEO

2016, http://dx.doi.org/10.1787/888933349957

Meanwhile, India has taken the lead over China

in terms of GDP growth (but not per capita), with favorable demographics that

encourage domestic savings and investment. In the future decades, Shifting

Wealth may well benefit from a twin-turbo, China and India. Twin-turbo refers to the turbocharger configuration in which two

identical turbochargers function simultaneously, splitting the turbocharging

duties equally. Each turbocharger is driven by half of the engine's spent

exhaust energy. A twin-turbocharger relying on China and India would be

good news for convergence and for the world economy, counteracting the backlash

emanating from populism and protectionism in the US and Europe.

Ever since the

1990s, there has been much talk about China´s growth slowing down. But China´s

slowdown has been overhyped in Western media recently, while India has been celebrated

as the new top-growth country. In per capita terms, however, China still leads

India. China´s growth has been coming

down from unsustainable levels, while India´s growth has been rising, erratically

so due to her exposure to weather conditions. In recent years, growth in both

Asian giants has comfortably settled above 5 percent per annum.

Figure

2: GDP real per

capita growth (annual %), 1990 - 2016

Source: https://data.worldbank.org/indicator/NY.GDP.PCAP.KD.ZG?end=2016&locations=CN-IN-1W&start=1990

The June 2017

issue of the World Bank´s Global Economic Prospects predicts real GDP growth at

6.3 percent for both 2018 and 2019; India´s growth is forecast to reach 7.5 and

7.7 percent, respectively, in the two forthcoming years. Current annual

population growth is 0.5 percent in China and 1.2 percent in India. So in real

terms, per capita income growth is forecast to be superior in India than in

China, albeit just by roughly half a percentage point.

Table 1: Percent of real global GDP

Growth, forecast 2017 – 2019

China

|

35.2

|

USA

|

17.9

|

India

|

8.6

|

EU

|

7.9

|

Indonesia

|

2.5

|

Brazil

|

1.2

|

Russia

|

1.0

|

Even so, Table 1

suggests that India is still far from contributing to global GDP growth on

equal terms with China. Mind you, India is forecast to contribute 8.6% to

global growth (based on the cited World Bank numbers), and that exceeds the EU

contribution. Meanwhile, China will support more than a third of world economic

growth during the end of the current decade.

For the moment, the world economy doesn´t enjoy a twin-turbo China-India quite yet. India is still too poor to meaningfully contribute: its GDP/capita relative to the USA stood at 11.6 percent in 2016. China´s per capita income stood at 26.7 percent of US mean per capita income (Figure3). Compared to the US, among the five BRICS countries only China and India have converged to US per capita income levels since 1990 and 2016.

Figure 3: Convergence to US GDP/cap, 1990-2016

Source: https://www.imf.org/external/pubs/ft/weo/2017/02/weodata/weoselgr.aspx

For the moment, the world economy doesn´t enjoy a twin-turbo China-India quite yet. India is still too poor to meaningfully contribute: its GDP/capita relative to the USA stood at 11.6 percent in 2016. China´s per capita income stood at 26.7 percent of US mean per capita income (Figure3). Compared to the US, among the five BRICS countries only China and India have converged to US per capita income levels since 1990 and 2016.

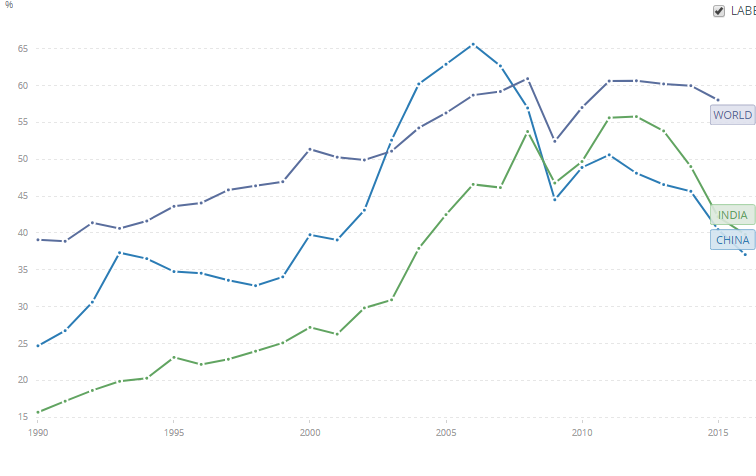

Figure 4: Trade (% of GDP)

Another concern

is that trade shares (% of GDP) have been dropping in India from 56 percent in

2012 to below 40 percent in 2016. India´s weak export performance reflects her

dependence on commodity exports and a poorly diversified export basket[2].

To be sure,

China´s trade shares have been dropping even more but this was a welcome

outcome of rebalancing the country toward more consumption. In any case, the

drop in trade shares observed in both Asian (Figure 3) giants translates

domestic GDP growth mechanically into lower contribution to global growth. The

twin-turbo support to the world economy in turn relies on an open trade system.

With the US retreat from multilateralism under Trump, the twin-turbo engine is

likely to stutter for a while.